Smarter Cars, Smarter Policies: IoT’s Impact on Auto Insurance

May 15, 2025

Introduction

The auto insurance industry is witnessing a paradigm shift after integration with connected vehicles and IoT technologies. These developments have made Usage-Based Insurance (UBI) possible, in which the premium determining factors are real-time driving behavior, as opposed to fixed variables like age and geography. In addition to improving pricing, IoT sensors benefit policyholders and insurers by improving fraud detection, claims processing, and road safety.

Standard insurance models often end up in generalized rates since they utilize broad risk estimations. On the contrary, insurers may monitor vehicle performance, fuel efficiency, and sensor data in real time with IoT-powered telematics, resulting in more precise risk assessment and customized insurance.

In this blog, we’ll look at how IoT-enabled telematics and linked car ecosystems are changing the auto insurance market. We will also explore the technologies causing these changes, their advantages for insurers and policyholders, and the associated ethical, legal, and regulatory issues. Regardless of whether you’re an insurer, a tech worker, or a policyholder eager to learn how IoT impacts your rates and protection, this blog will provide insightful information about the future of smarter, more equitable, and more connected auto insurance.

Thanks to IoT-enabled technologies, connected vehicles can use Vehicle-to-Everything (V2X) communication protocols to interact with their environment. This comprises internet of things platforms, communication protocols for engaging with pedestrians (V2P), cloud computing systems (V2C), and other vehicles (V2V).

IoT-Enabled Features in Modern Cars

- GPS Tracking & Navigation – Offers real-time location information, aiding navigation and fleet management while reducing energy consumption.

- Black Box Telematics – Monitors driving trends that insurers use in calculating Usage-Based Insurance (UBI) premiums.

- AI-Powered Dashboards – Utilizes machine learning to detect patterns in driving trends, device data, and maintenance demands.

The Role of IoT in Auto Insurance

- IoT-Enabled Data Collection & Telematics: In an effort to gauge risk and enhance policy offerings, insurers use real-time device data obtained from IoT sensors and telematics.

- Usage-Based Insurance (UBI): Insurance companies can base rates on a driver’s driving habits thanks to IoT-driven PAYD and PHYD models.

- Personalized Premiums: Data generated by AI dynamically updates insurance pricing, guaranteeing that safer drivers pay less.

- Enhanced Risk Assessment: IoT applications produce accurate risk profiles through big data analytics and AI-driven predictive models.

- Automated Accident Detection: IoT-enabled sensors can detect vehicle performance issues and notify insurers for smart claims processing.

- Remote Vehicle Diagnostics: IoT-based remote monitoring improves predictive maintenance, reducing human intervention in vehicle upkeep.

- Smart Claims Processing: IoT device management enhances fraud detection, streamlining settlements with secure IoT protocols.

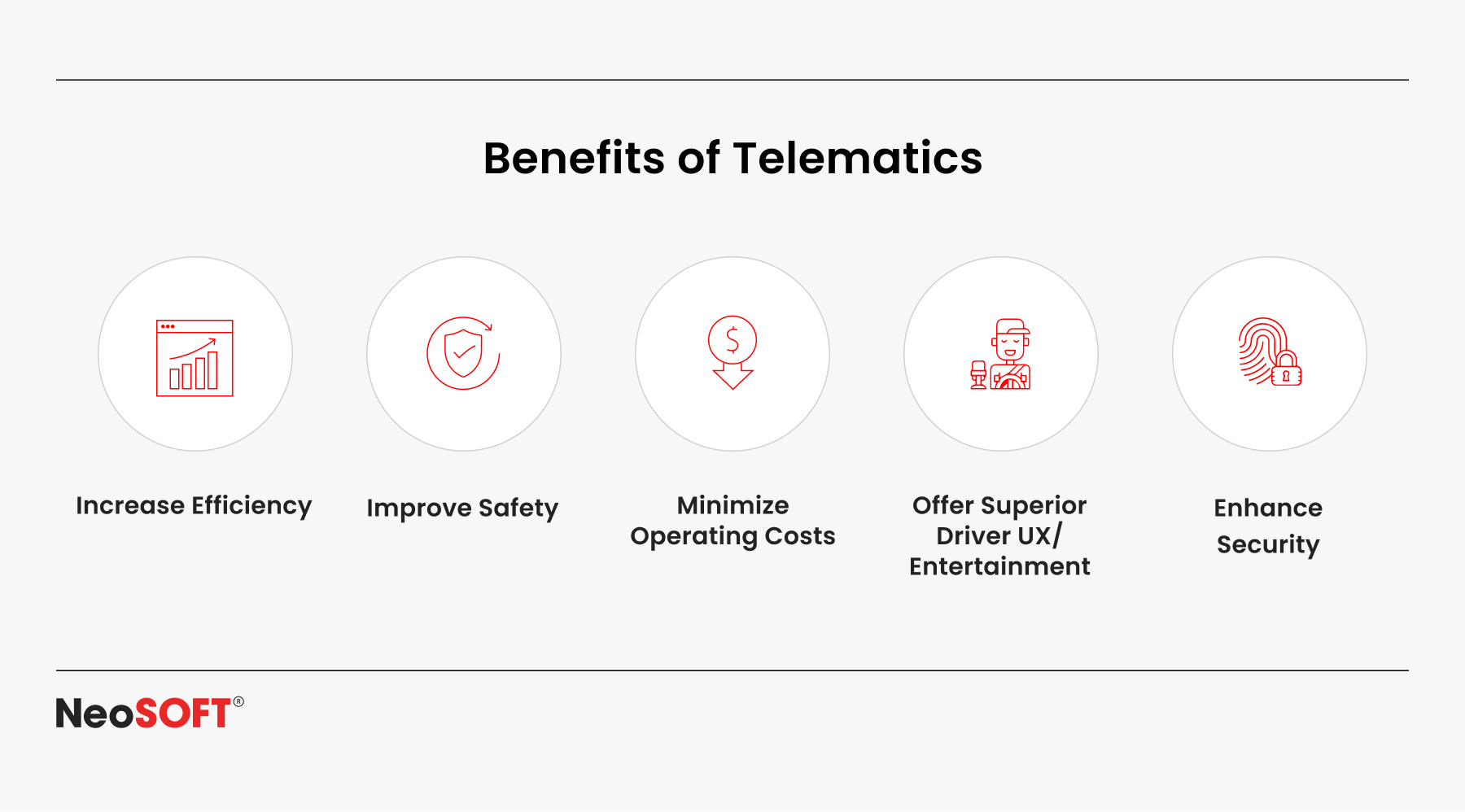

Key Benefits of IoT-Driven Auto Insurance

The primary benefits of IoT-driven auto insurance include:

Fair & Personalized Pricing

Standard healthcare models, which determine costs on key hazards like gender, residence, and vehicle type, can sometimes lead to inaccurate or generic pricing. Insurance companies may track information from sensors, vehicle performance, fuel efficiency, and driving habits in real time with IoT-powered telematics offering dynamic and reduced pricing. Sensor data is gathered using IoT applications and connected devices to make sure consumers pay insurance based on real hazards rather than presumptions.

Fraud Detection & Prevention

Auto insurance fraud is a significant concern, since it has caused insurers to forfeit billions. IoT security systems enhance fraud prevention by ensuring the authenticity of collected data. IoT-enabled fraud detection uses artificial intelligence and machine learning to detect patterns in accident reports, sensor data, and device data to identify suspicious claims. With IoT networks supporting secure data exchange, fraudulent claims can be flagged before payouts, reducing financial losses and ensuring fair settlements.

Faster Claims Processing

Lengthy evaluations and human verifications are common reasons why claim payouts in conventional insurance models are frequently delayed. Using automated IoT solutions such as powered by blockchain network protocols, which guarantee safe and effective data transmission between insurance companies, claim adjusters, and policyholders, IoT-connected platforms expedite the claims processing process.

Instant communication of accident details via IoT devices reduces human intervention and speeds up claim approvals. Long-term investigations are no longer necessary because insurers may obtain real-time accident data from IoT sensors and smart devices.

Encouraging Safer Driving Habits

Insurers provide real-time driver feedback through wearable technology, smart objects, and Internet of Things-enabled telematics with the purpose of reducing hazardous driving behavior like speeding, assertive braking, and distracted driving. Certain IoT solutions combine with graphical user interfaces (GUIs) to give drivers information about their driving enabling them to make safer judgments while driving.

Predictive Maintenance & Safety Alerts

IoT sensors and industrial IoT devices analyze mechanical parts such as automobile tires, brakes, and engines to detect early indicators of wear and tear. Proactive maintenance systems reduce the probability of malfunctions by generating safety signals before concerns escalate. Using IoT data, insurers may also recommend the best energy management strategies to boost fuel economy and keep linked cars in top shape.

The integration of IoT technologies into insurance benefits both insurers and policyholders by creating a more transparent, secure, and efficient system. As IoT deployments grow, auto insurers must embrace internet of things innovations to remain competitive in a connected vehicle ecosystem.

The Role of Edge Computing in IoT-Based Auto Insurance

Vast amounts of instantaneous data is developed by IoT devices, making conventional cloud computing susceptible to security threats and latency issues. Instead of depending entirely on remote cloud servers, edge computing handles these issues by analyzing information closer to the source, such as within cars or adjacent nodes in the network.

Edge computing permits insurers to conduct risk assessment, fraud detection, and premium adjustments in real-time without being delayed by network outages Furthermore, by improving data security and privacy edge based IoT applications lower the possibility of cyberattack on centralized insurance networks. By utilizing AI-powered edge analytics, insurers may provide more personalized and faster claims processing making the industry more efficient and customer-focused.

The Ethical & Legal Implications of IoT in Auto Insurance

Considerations of ownership, confidentiality of information, and regulatory compliance are brought up by the use of IoT in auto insurance. Insurers companies’ real-time data gathering on driving patterns, car location, and even biometric information may give rise to concerns about authorization, monitoring, and inherent biases caused by algorithms in pricing. Consumers worry about unfair premium hikes, lack of control over personal information, and misuse of data.

Insurers must place stringent data protection strategies, ensure transparency in data usage, and adhere to compliance regulations like the GDPR, and CCPA to mitigate these concerns. Encrypted data storage and transparent opt-in methods will be crucial in maintaining consumer confidence while striking a balance between innovation and moral obligation.

Impact on Insurance Companies

The transition from conventional insurance policies to based on data IoT deployments is changing the business models of insurers as a result of the widespread utilization of IoT solutions. IoT security measures increase profitability by lowering the number of false claims.

Further, IoT connectivity improves customer happiness and reduces administrative expenses by simplifying smart claims processing. By implementing cutting-edge solutions like pay-per-mile insurance and connecting with power management systems to maximize vehicle economy, insurers using IoT platforms obtain a competitive advantage.

Consumer Perspective

IoT-powered smart insurance provides advantages to customers like remote monitoring, customized pricing, and quicker claims resolution. Insurance becomes more equitable when IoT standards allow policyholders to optimize energy usage. Consumer worries about privacy and ongoing data interchange, however, are still very real.

Some insurers offer opt-out options for IoT tracking, but these often result in higher premiums. To encourage adoption, insurers must ensure transparent IoT device data policies and use GUIs that help users understand their insurance benefits easily.

IoT-Driven Pay-Per-Mile Insurance: A Game Changer?

Even in cases where the vehicle is not used frequently, conventional auto insurers have set premiums. IoT-enabled pay-per-mile insurance (PPMI), has altered this narrative by basing rates on actual mileage and driving patterns.

Urging safer behavior, PPMI reduces accident claims, and helps low-mileage drivers save money. However the pricing may differ and the continuous surveillance may arouse a sense of unease. Despite these drawbacks, IoT-powered PPMI is reshaping insurance by making it more flexible and usage-based for contemporary drivers.

Challenges & Solutions

IoT-driven auto insurance has many benefits but in order to be widely adopted to succeed in the longer run, insurers have to address a number of obstacles like:

1. Privacy & Data Security

Real-time driving data collection may raise significant concerns pertaining to user privacy and data ownership, including:

- Policyholders may become aware of insurers tracking their whereabouts and driving behavior, undermining their faith.

- Sensitive intimate and vehicle information may be exposed due to the possibility of security breaches or illegal access.

- Legal disagreements over control and usage of acquired data may result from unclear data ownership policies.

Solution: Building consumer trust demands insurers to conform to regulatory norms, build robust encryption systems, and assure transparent data usage rules.

2. Customer Acceptance:

Despite the advantages of IoT-based insurance, consumer skepticism remains a barrier:

- Some drivers fear that minor infractions could lead to sudden premium increases.

- Policyholders may be deterred from establishing telematics-driven policies due to worries about ongoing monitoring.

- Reduced acceptance rate due to non-tech savvy consumers, especially the older demographics.

Solution: Insurance companies ought to focus on informing customers about advantages of IoT & improvement of equity and safety. Also, early adopters should be rewarded with incentives to curb these issues.

3. Legal & Regulatory Concerns:

Legal complexities caused due to different regions having varying regulations on telematics and data sharing practices:

- Securing a balance between technological innovation & consumer protection requires continuous regulatory evolution.

- Adherence to laws such as GDPR (Europe), CCPA (California), and other data securing regulations to ensure ethical data collection.

- Following strict privacy regulations when data is shared between automakers, insurers, and third-party service providers.

Solution: Collaboration between automakers, insurers, and policymakers is essential to establish transparent standardized regulations that boost innovation while safekeeping consumer rights.

4. Technology Barriers:

- High Implementation Costs: Costing a fortune to deploy IoT infrastructure, such as data analytics, telematic devices, and AI-driven risk assessment systems.

- Integration Challenges: Integrating existing insurance systems with IoT solutions can be tedious and resource-intensive.

- Limited Accessibility: Little to no access of IoT-based policies to vehicle owners with

older models lacking built-in connectivity.

Solution: Insurers can decrease costs and improve scalability by collaborating with smart city initiatives, automakers, and tech companies to create shared data ecosystems improving affordability.

The Future of IoT in Auto Insurance

The future of IoT-driven auto insurance is centered on connectivity technologies, AI, and blockchain for fraud-resistant IoT applications.

- AI & Machine Learning for Smarter Risk Assessments: IoT-driven artificial intelligence will refine sensor data analysis to improve pricing accuracy.

- Blockchain for Secure Data Management: IoT ecosystems will use IoT security protocols for tamper-proof records of accident history and claims.

- Autonomous Vehicles & Smart City Integration: IoT-connected vehicles will interact with smart cities through communication protocols for seamless insurance adjustments.

- 6G Connectivity & Edge Computing: The emergence of 6G networks will enable instantaneous data transmission from IoT devices, improving real-time risk assessment and policy adjustments.

- Quantum Computing in Insurance: Future quantum algorithms could enhance fraud detection by analyzing vast amounts of insurance data faster than classical systems.

- Ethical AI & Fair AI Practices: Insurers need to eliminate algorithmic biases as AI-driven screening becomes increasingly prevalent in order to avoid unfair premium hikes based on demographics.

Conclusion

IoT-powered telematics and correlated car ecosystems are driving a significant revolution in the auto insurance sector. In addition to offering policyholders individualized pricing, increased transparency, and enhanced road safety, these technologies are changing how insurers evaluate risk, identify fraud, and handle claims.

These developments also bring with them important problems, such as worries about data privacy, unclear regulations, and the moral application of AI to insurance decision-making. To ensure a sustainable, safe, and customer-friendly insurance model, these problems must be resolved.

As IoT continues to transform the industry landscape, companies must proactively embrace innovation, compliance with regulations, and responsible data governance. In order to make well-informed judgments, consumers should educate themselves on how IoT-driven rules affect their personal data, driving behavior, and premiums.

Those that can effectively strike the equilibrium between data security, technical developments, and ethical considerations will influence the foreseeable future of vehicle insurance. Now is the moment to act, whether you’re a customer navigating a changing environment or an insurer adjusting to new business models. Will you welcome the transition to an insurance environment that is more intelligent, equitable, and interconnected?

Access the future of more intelligent, secure, and individualized auto insurance with the aid of our IoT and AI-powered insurance products. Contact us at info@neosofttech.com to learn how our intelligent data systems and connected car platforms may reinvent your insurance packages and build consumer confidence.

Up Next

Enterprise AI Adoption: The Gap Between Using AI and Running on AI Is Where Most Companies Will Lose

Up Next

Still Processing Claims Manually? Why Insurance Claims Automation Is Transforming the Industry

Recommended